Commercial Real Estate Crisis: Can it Damage the Economy?

The commercial real estate crisis looms as a significant challenge in 2024, threatening to reshape the landscape of urban economies. With high office vacancy rates—often exceeding 23% in key markets like Boston—the repercussions are substantial, including a dramatic decrease in property values. Experts like Kenneth Rogoff warn that as a wave of real estate loans matures by 2025, the risk of bank failures could escalate, particularly among smaller institutions that remain vulnerable. Compounded by the lingering effects of the pandemic and rising interest rates, the potential for a broader financial crisis becomes a topic of heated debate among economists and investors alike. As stakeholders brace for a turbulent market, understanding these dynamics is crucial for navigating the uncertain future of commercial real estate.

Navigating the present turmoil in commercial property markets reveals a precarious situation for investors and local economies alike. The sudden increase in office space vacancies, compounded by the fallout from the pandemic, raises critical concerns about the stability of commercial real estate investments. Commentators, including noted economist Kenneth Rogoff, predict that significant delinquencies on real estate loans could lead to cascading effects in the banking sector, particularly affecting regional banks with heavy exposure to real estate collateral. As the market grapples with looming financial pressures, the economic repercussions could echo beyond just the property sector, influencing bank operations and lending practices. Overall, the intricate web of office spaces, bank liquidity, and financial regulations is vital for understanding today’s economic landscape.

The Impact of High Office Vacancy Rates on the Economy

High office vacancy rates pose a significant economic challenge as they reflect a stark shift in the demand for commercial real estate stemming from the pandemic. Major cities, like Boston, report vacancy rates between 12 to 23 percent, representing a drastic downturn in property values. This substantial decrease not only impacts landlords and investors but also reverberates through local economies, as businesses shedding office space often lead to reduced spending in nearby areas. The ripple effects can dampen job growth and slow recovery in sectors reliant on commercial activity, making it crucial for policymakers to address the underlying issues driving these vacancy rates to stabilize the economy.

Moreover, the long-term implications of sustained high office vacancy rates could lead to broader financial repercussions, particularly as significant commercial mortgage loans come due. If property owners struggle to refinance due to declining values and rising interest rates, we may witness a heightened risk of defaults. This potential scenario is particularly concerning as commercial real estate loans constitute a substantial portion of lenders’ assets. Should these defaults increase, it could have a cascading effect on financial institutions that are already grappling with the fallout from recent bank failures and uncertainties in the real estate market.

The Looming Commercial Real Estate Crisis

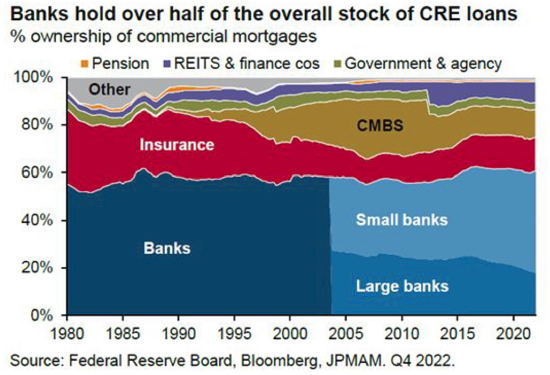

The looming commercial real estate crisis is characterized by a significant wave of loans maturing soon, which could exacerbate existing vulnerabilities in the banking system. As Kenneth Rogoff pointed out, 20 percent of the $4.7 trillion in commercial mortgage debt is set to mature this year, raising alarming concerns about the potential for widespread bank failures if businesses default on their loans. The repercussions could be far-reaching, leading to a decline in consumer confidence and increased restraint in lending practices. Economic growth may stall as banks tighten their lending terms in response to losses from underperforming real estate assets.

In an environment where office vacancy rates remain historically high, the outlook appears uncertain for many commercial properties. Investors may find themselves in a precarious position, particularly those who over-leveraged during periods of low interest rates. The potential for significant equity losses in commercial real estate could have lasting impacts beyond the sector itself, potentially necessitating further regulatory scrutiny and intervention from federal authorities. As we approach 2025, vigilance in monitoring these developments will be essential to preempt more severe financial crises.

Navigating Bank Failures in the Commercial Real Estate Sector

The threat of regional bank failures tied to the commercial real estate sector cannot be understated, especially as many smaller institutions are more exposed due to less stringent regulations. The need for robust financial health is paramount, yet many of these banks heavily invested in commercial properties now face the brunt of high vacancy rates and dwindling property values. As bank failures in the past have shown, rapid interventions are required to stabilize the financial system. The Federal Reserve has previously stepped in to mitigate losses, but the sustainability of such measures raises concerns about long-term fiscal responsibility and market confidence.

If several regional banks falter due to a spike in delinquent commercial real estate loans, it could worsen the overall financial landscape, leading to stricter lending practices and decreased credit availability for consumers and businesses. This tightening could stifle economic recovery efforts, particularly in vulnerable areas already struggling to bounce back from the pandemic’s economic repercussions. The ripple effects of such failures could extend beyond the banking community, influencing broader economic conditions.

The Role of Interest Rates in the Commercial Real Estate Landscape

Interest rates play a critical role in shaping the commercial real estate market dynamics, and their current trajectory has significant implications for property investors. After prolonged periods of low interest rates, many investors became accustomed to accessible financing, leading to high levels of leverage. However, the recent increases in rates have caught many off guard, with growing concerns about the sustainability of their investments when loan terms become less favorable. Economists like Kenneth Rogoff suggest that unless we experience a severe recession that drives rates down again, many investors could face harsh realities as their refinancing options dwindle.

The impact of interest rates is also visible in how banks assess risk and allocate resources. With significant portions of their assets tied up in commercial real estate loans, banks may need to recalibrate their strategies as borrowers struggle to meet repayment expectations. A proactive approach, guided by prudent lending practices, is essential to mitigate the effects of rising rates on the broader economy. This nuanced balance between managing interest rates and supporting economic growth defines the challenges ahead for financial institutions and the commercial real estate sector.

Understanding Bank Regulations in the Wake of the Financial Crisis

The aftermath of the 2008 financial crisis led to significant regulatory reforms that today shape the resilience of major banks amidst rising commercial real estate concerns. Stricter capital requirements and oversight mean that larger banks like Citigroup and JPMorgan Chase are better positioned to withstand shocks from their commercial real estate portfolios. These measures have fortified their balance sheets, allowing them to navigate through downturns more effectively than smaller banks that didn’t face the same regulatory scrutiny. Consequently, while smaller institutions may be more vulnerable to current crises, larger banks still enjoy a comparatively stable footing in the marketplace.

However, the challenge remains that ongoing vulnerabilities within regional banks could exacerbate localized economic issues, particularly if a string of bank failures occurs. As we’ve seen, the investments made by regional banks in commercial real estate are pivotal for community financing; hence, any significant disturbance can impact local economies. While the risks associated with these smaller banks are concerning, the larger banking entities’ diversified asset management can help cushion broader economic impacts. Understanding the intricate relationship between regulation, market dynamics, and credit availability is critical in analyzing the evolving landscape of commercial real estate.

Long-term Strategies to Address Commercial Real Estate Challenges

To mitigate the economic impact of high office vacancy rates and looming commercial real estate crises, long-term strategies must be a priority for stakeholders. Addressing the underlying issues that contribute to low demand for office spaces, such as remote work trends and shifting employee preferences, presents an opportunity to rethink how commercial properties are utilized. Implementing flexible leasing options and repurposing unused spaces to meet evolving demands could help revitalize the market while simultaneously ensuring that property values stabilize. Such transitional strategies will be paramount for attracting tenants, enhancing the desirability of once-struggling office buildings.

Engaging in multi-stakeholder collaborations—bringing together financial institutions, urban planners, and local governments—can foster innovative solutions that enhance the resilience of commercial real estate markets amidst uncertainties. Promoting sustainable development practices and leveraging technology can also play a transformative role in attracting businesses back to physical office spaces. By proactively addressing these challenges and fostering a shared vision of future real estate landscapes, we can work towards reducing vacancy rates and reinforcing the foundations of local economies.

Consumer Confidence Amidst Rising Economic Uncertainty

Consumer confidence remains a pivotal aspect of economic recovery, particularly in light of rising interest rates and the specter of potential bank failures. While many sectors of the economy demonstrate resilience, the commercial real estate market’s struggles can create tension that undermines overall confidence. Concerns about financial stability may lead consumers to curtail spending, which in turn can stifle growth and recovery efforts. Therefore, restoring trust and ensuring that consumers feel secure in their financial choices is crucial to maintaining a buoyant economic environment as external pressures mount.

As experts continue to monitor the banking sector’s health, the interplay between consumer sentiment and economic stability will undoubtedly influence how markets react to ongoing developments. Building confidence among consumers will require transparent communication from financial institutions and policymakers to assure them of a managed approach to emerging challenges. Encouraging responsible lending practices and emphasizing financial literacy can also empower consumers to make informed decisions, ensuring they remain optimistic amidst uncertainty.

The Global Context of the Commercial Real Estate Market

The commercial real estate crisis in the U.S. cannot be viewed in isolation; a global perspective reveals that other markets similarly grapple with challenges stemming from changing economic landscapes. While U.S. cities face significant office vacancy rates, some European markets showcase differing resiliency due to unique work-life dynamics and cultural values surrounding office work. Understanding these international parallels allows investors and policymakers to glean insights into how different regions manage their commercial real estate challenges while adapting to changing demands.

Moreover, as countries across the globe contend with the repercussions of the pandemic and shifting economic paradigms, the interconnectedness of the financial systems means that crises in one region can create ripple effects elsewhere. The potential for defaults in commercial real estate can influence global markets, especially in nations with heavily interconnected banking systems. By assessing the broader economic context, stakeholders can better position themselves to navigate the complexities of the commercial real estate landscape and devise strategies that account for both local and international dynamics.

Frequently Asked Questions

How are high office vacancy rates affecting the commercial real estate crisis in the U.S.?

High office vacancy rates are significantly contributing to the commercial real estate crisis by decreasing property values and increasing the risk of delinquent loans. As businesses continue to adopt remote and hybrid work models, demand for downtown office space has plummeted, leaving many buildings with vacancy rates soaring between 12% and 23% in major cities. This drop in occupancy is leading to financial strain on property owners and lenders, raising concerns about potential bank failures within the sector.

What role do bank failures play in the commercial real estate crisis?

Bank failures may play a crucial role in exacerbating the commercial real estate crisis, particularly as a large number of real estate loans are scheduled to mature by 2025. If a significant wave of commercial mortgage delinquencies occurs, smaller and medium-sized banks that are heavily invested in real estate could face substantial losses, potentially leading to failures. While larger banks are generally more resilient due to strict regulations and diversified portfolios, the impact of regional bank failures could still ripple through the economy.

What are the implications of rising interest rates on the commercial real estate crisis?

Rising interest rates have serious implications for the commercial real estate crisis, as many investors initially over-leveraged during periods of low rates. As rates increase, refinancing options become more challenging, making it difficult for property owners to manage debts. This can lead to higher office vacancy rates and increased delinquency on commercial real estate loans, which in turn may threaten the stability of regional banks invested in those properties.

According to Kenneth Rogoff, will the commercial real estate crisis lead to a financial meltdown?

Kenneth Rogoff suggests that while the commercial real estate crisis could result in significant losses for investors and some regional banks, it is unlikely to lead to a full-blown financial meltdown akin to the 2008 crash. He highlights that most major banks are better regulated and diversified now, reducing the risk of widespread financial collapse. However, the situation is precarious and could change if additional economic challenges arise.

What structural issues contribute to the commercial real estate crisis in converting office spaces?

The commercial real estate crisis is further complicated by structural issues in converting vacant office spaces into residential apartments. Many office buildings are ill-suited for such transformations due to zoning laws, lack of windows, low ceilings, and poorly positioned infrastructure, making it costly and challenging to repurpose them for residential use. This limitation prolongs the impact of high office vacancy rates on the market.

What impact does the commercial real estate crisis have on consumers and the broader economy?

The commercial real estate crisis may harm consumers primarily through potential losses to pension funds that invest in the sector. Regional banks facing losses could tighten lending standards, affecting consumer spending. However, the broader economy appears stable due to a strong job market and thriving stock market, suggesting that while commercial real estate is facing significant challenges, the overall economic impact may not be as severe.

Can long-term interest rates collapsing mitigate the commercial real estate crisis?

A collapse in long-term interest rates could indeed help mitigate the commercial real estate crisis by easing refinancing challenges for property owners. Cheaper borrowing costs might stimulate the market, allowing distressed assets to stabilize. However, analysts view this scenario as unlikely unless a severe recession occurs that substantially alters the financial landscape.

What are the potential consequences of regional banks failing in the context of the commercial real estate crisis?

If regional banks fail due to the commercial real estate crisis, it could lead to localized economic disruptions, affecting lending and consumption in those areas. The failure of smaller banks poses less of a systemic risk compared to larger financial institutions like Bank of America or JPMorgan Chase, but nevertheless, these failures may impact the trust and stability within the bank lending ecosystem.

| Key Point | Details |

|---|---|

| High Vacancy Rates | Downtown office space vacancy rates in major U.S. cities, including Boston, range from 12% to 23%, leading to reduced property values. |

| Upcoming Loan Maturities | 20% of $4.7 trillion in commercial mortgage debt will mature this year, raising concerns about defaults. |

| Risk of Bank Failures | Federal regulations are stronger for large banks, but smaller banks may face significant risks due to their exposure to commercial real estate. |

| Economic Impact | Some losses in commercial real estate will affect consumers and local economies, even as the broader economy remains robust. |

| Potential for Recovery | The presumption by investors that interest rates will decline may offer some hope for recovery in the sector. |

| Challenges of Conversion | Transitioning vacant office buildings into residential units faces complications due to zoning and building standards. |

Summary

The commercial real estate crisis poses significant risks to the economy, particularly as high office-vacancy rates and maturing loans threaten financial stability. While experts believe a widespread meltdown is unlikely, the vulnerability of smaller banks and the potential impact on consumers highlight the need for strategic intervention. Investors in commercial real estate are holding their breath for potential interest rate declines, which could alleviate some pressure. However, without addressing structural issues in the market, the sector may continue to grapple with significant challenges.